Managing Formulary Changes: How to Handle Prescription Drug Coverage Updates

Jan, 3 2026

Jan, 3 2026

What Is a Formulary, and Why Does It Matter?

A formulary is the list of prescription drugs your health plan covers - and how much you pay for each one. It’s not just a catalog. It’s a financial and clinical tool that decides which medications you can get, at what cost, and under what rules. Most plans use a tiered system: Tier 1 might be generic drugs costing $10, Tier 3 could be brand-name drugs costing $100, and Tier 5 or 6 might be specialty drugs like Humira or Enbrel, where you pay 30-40% of the price out of pocket.

Formularies exist because drug prices are skyrocketing. In 2023, U.S. spending on prescription drugs hit $621 billion. Without formularies, insurance plans would be overwhelmed. But the trade-off is real: when a drug moves from Tier 2 to Tier 3, your monthly cost can jump from $50 to $650 overnight. That’s not hypothetical. In 2024, a Reddit user reported their Humira cost went from $50 to $650 after their plan changed its formulary - and they had to fight for three weeks just to keep their medication.

How Formulary Changes Happen - And When You’ll Find Out

Formularies aren’t set in stone. Every year, pharmacy and therapeutics (P&T) committees - made up of doctors, pharmacists, and sometimes patient reps - review which drugs stay, go, or move tiers. They look at clinical data, price negotiations, and rebates from drugmakers. Most large insurers review their formularies quarterly. Medicare Part D plans must notify you 60 days before any non-urgent change. Commercial plans? Often just 22 days. And here’s the problem: 57% of patients say they get no clear notice at all.

Changes can happen mid-year. A drug might get pulled because a cheaper generic came out. Or a brand-name drug might be moved to a higher tier because the manufacturer refused to give a bigger discount. Sometimes, a drug is removed entirely - no warning, no grace period. That’s when patients panic. They’ve been on the same medication for years. Suddenly, it’s not covered. They don’t know what to do next.

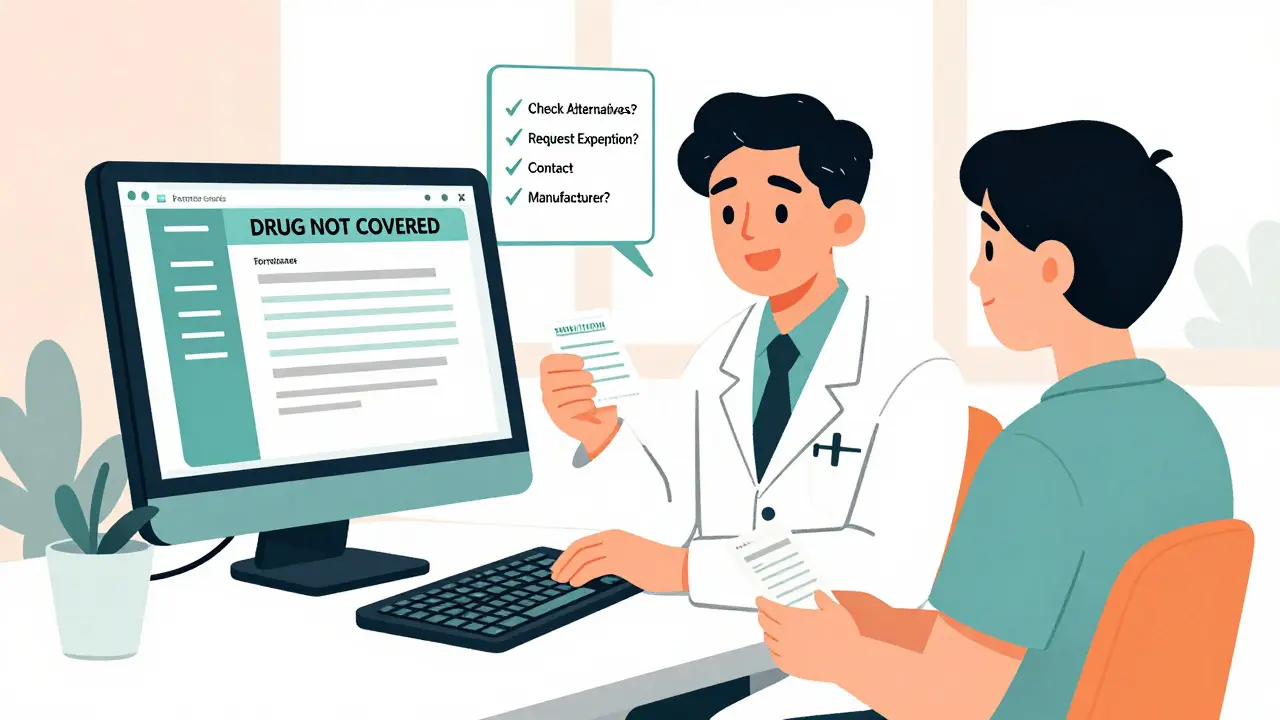

What to Do When Your Drug Is Removed or Moved

If your medication is taken off the formulary or moved to a higher tier, you have options - but you need to act fast.

- Check for alternatives. Your doctor can often switch you to another drug in the same class. For hypertension, there are eight common generics. For diabetes, there are at least five alternatives to a discontinued brand. Ask: “Is there another drug that works just as well, and is still covered?”

- Request a formulary exception. This is a formal appeal. You or your doctor submits documentation showing why you need the drug - maybe you tried alternatives and had side effects, or your condition is unstable without it. According to CMS data, 64% of medically justified exceptions are approved. Don’t assume it’s denied.

- Use manufacturer assistance. Many drugmakers offer copay cards or free medication programs. In 2024, these programs covered $6.2 billion in patient costs. For drugs like Humira or Enbrel, you might pay $0 after applying.

- Switch plans during open enrollment. If you’re on Medicare, use the Plan Finder tool. If you’re on employer insurance, wait for your next enrollment period. Don’t wait until your drug is gone to shop around.

How Providers Are Handling This - And How You Can Benefit

Good clinics don’t wait for patients to show up confused. They monitor formulary changes proactively. About 76% of large medical groups now use e-prescribing systems that check coverage in real time. When a doctor writes a prescription, the system flags if the drug is no longer covered or needs prior authorization. That means you get a call before you even get to the pharmacy.

Some practices send out alerts 60 days before changes take effect. One nurse on AllNurses shared how her clinic does it: “We switch patients during routine visits. No disruption. No panic.” That’s the gold standard. If your provider doesn’t do this, ask them to. You have a right to be prepared.

Medicare Part D vs. Commercial Plans - Key Differences

Medicare Part D plans have stricter rules than commercial insurance. They must cover at least two drugs in every therapeutic class. They can’t drop a drug without 60 days’ notice. They must allow a 30- to 60-day transition supply if you’re already taking it. And they’re required to process urgent exception requests within 72 hours.

Commercial plans? No such guarantees. They can remove a drug with as little as 10 days’ notice. They often use “accumulator adjustment” programs - where manufacturer coupons don’t count toward your deductible. That means you might think you’re saving money, but you’re actually hitting your out-of-pocket maximum slower. In 2025, 71% of commercial plans will use these programs. Medicare Part D plans are catching up - 43% now do too.

How Formulary Changes Affect Real People

It’s not just about money. It’s about health.

A 2023 Scripta Insights report found that 22% of patients stop taking their meds because of formulary changes. For diabetes patients, that number jumps to 58%. Why? When a drug moves from Tier 2 to Tier 3, abandonment rates spike by 47%. People choose between food, rent, and insulin. That’s not a choice anyone should have to make.

Low-income Medicare beneficiaries are hit hardest. A 2023 JAMA study showed that excessive formulary restrictions led to a 12% increase in emergency room visits among this group. They couldn’t afford their meds. Their condition worsened. They ended up in the ER - which costs far more than the drug ever did.

On the flip side, value-based formularies - which reward drugs that actually improve outcomes - are reducing total healthcare costs by 9-14%. These systems are rare now, but growing. By 2027, 45% of employer plans are expected to use them. That’s the future: paying for results, not just pills.

What You Can Do Now - Before It’s Too Late

Don’t wait for a letter from your insurer. Take control.

- Check your formulary every year. During open enrollment, log into your plan’s website. Search every drug you take. Note the tier and any prior authorization rules.

- Save your coverage documents. Keep a printed or digital copy of your current formulary. When changes come, compare them side by side.

- Know your appeal rights. Every plan has a process. Know the deadline. Know who to call. Medicare beneficiaries get extra help from SHIP (State Health Insurance Assistance Programs) - and those who use it have a 37% higher success rate on appeals.

- Ask your pharmacist. They see formulary changes every day. They know which drugs are being pulled and what alternatives are covered.

The Bigger Picture: Where Formularies Are Headed

Formularies aren’t going away. But they’re changing. The next wave is personalization. By 2035, experts predict “individualized formularies” based on your genetics, past treatment response, and even your lifestyle. AI tools already predict with 89% accuracy which patients will stop taking a drug if it’s moved to a higher tier.

The Inflation Reduction Act caps out-of-pocket drug costs at $2,000 a year for Medicare beneficiaries starting in 2025. That’s huge. It means insurers can’t push patients into financial ruin anymore. That will force formularies to become smarter - not just cheaper.

But transparency remains a problem. Only 22% of patients understand how decisions are made. If your plan removed a drug and didn’t explain why, you’re not alone. Demand better communication. Ask for the clinical rationale. Ask who decided. And if you’re ignored - speak up. Your health depends on it.

What should I do if my medication is removed from my formulary?

First, check if there’s a similar drug still covered. Ask your doctor for alternatives. Then file a formulary exception request - 64% of these are approved if you provide medical justification. You can also contact the drug manufacturer for patient assistance programs. Don’t stop taking your medication until you have a plan.

How much notice do insurers have to give before changing my drug coverage?

Medicare Part D plans must give you 60 days’ notice for non-urgent changes. Commercial plans are not required to give any minimum notice, but most provide 22-30 days. Always check your plan’s documents - some offer more. If you get less than 10 days, you may have grounds to appeal.

Can I switch plans mid-year if my drug is dropped?

Generally, no - unless you qualify for a Special Enrollment Period. For Medicare, this includes moving to a new home, losing other coverage, or if your plan stops offering coverage in your area. For employer plans, you can only switch during open enrollment or after a qualifying life event like marriage or birth of a child. Don’t wait - plan ahead during annual enrollment.

Why do some drugs get removed from formularies?

Drugs are removed for three main reasons: 1) A cheaper generic becomes available, 2) The manufacturer didn’t offer a good enough discount, or 3) New clinical evidence shows another drug works better or has fewer side effects. It’s rarely about safety - it’s about cost and value.

Are generic drugs always better than brand-name drugs?

For most medications, yes - generics are chemically identical and just as effective. But for some complex drugs - like biologics used for autoimmune diseases - the differences can matter. If you’ve been stable on a brand-name drug for years, switching to a biosimilar might not be safe. Always talk to your doctor before switching.

What’s the difference between a tiered and a closed formulary?

A tiered formulary puts drugs into cost levels (Tier 1, Tier 2, etc.) and lets you choose from many options - you just pay more for higher tiers. A closed formulary only covers a limited list of drugs - often just generics - and won’t cover anything outside it unless you get an exception. Closed formularies save money but limit choices.

How can I find out if my plan’s formulary is changing?

Check your plan’s website during open enrollment. Look for a “Formulary Update” or “Drug List Change” notice. Sign up for email alerts if available. Call your insurer directly and ask: “Will any of my medications be affected next year?” Don’t rely on mail - many people never receive these notices.

Ian Detrick

January 5, 2026 AT 01:00Brittany Wallace

January 5, 2026 AT 01:29Michael Burgess

January 5, 2026 AT 13:05Lori Jackson

January 6, 2026 AT 13:50Sarah Little

January 8, 2026 AT 05:27innocent massawe

January 8, 2026 AT 06:41JUNE OHM

January 8, 2026 AT 16:51Philip Leth

January 9, 2026 AT 10:11Shanahan Crowell

January 10, 2026 AT 00:48